World Economy Has Record-High Protection Gap of $1.2 Trillion

September 09, 2019

The world economy is less resilient now than in 2007 at the onset of the global financial crisis, according to the new Macroeconomic Resilience Indices jointly developed by Swiss Re Institute (SRI) and the London School of Economics (LSE).

By contrast, separate insurance resilience indexes show that the resilience of households against three main areas of risk—natural catastrophes, mortality, and healthcare spending—has improved in most regions since the turn of the century, according to the latest sigma report.

Insurers could boost global financial resilience by closing a record-high $1.2 trillion composite protection gap for the three areas of risk, said Swiss Re.

"It is a trillion-dollar opportunity for the insurance industry," said Jerome Jean Haegeli, group chief economist at Swiss Re. "The insurance industry has largely kept pace with growing loss potentials and can do more to improve resilience. Emerging markets, in particular, benefit more strongly from insurance protection than mature economies, which often have greater access to alternative sources of funding."

A Holistic View at Macroeconomic Resilience

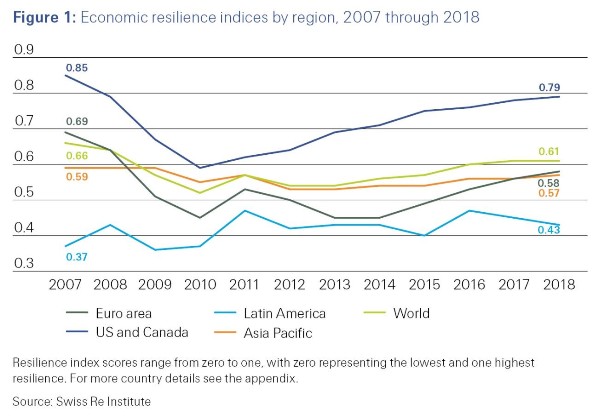

The new macroeconomic resilience indexes use data from 2007 to 2018 for 31 countries, representing about 75 percent of the world gross domestic product (GDP). The analysis shows that 80 percent of the sample countries had lower resilience scores in 2018 than in 2007. The main drivers of this trend have been exhaustion of monetary policy options in many developed economies and a challenging operating environment for the banking sector, even as financial institutions are stronger since the crisis.

"Considering the 35 percent probability of recession in the US next year and the global ramifications thereof, it is more important than ever to assess the underlying resilience of our economies and look beyond the traditional GDP measures," Mr. Haegeli continued. "In aggregate, policy buffers against economic shocks today are thinner than in 2007. Ultra-accommodative monetary policy over the past years leaves limited future room to maneuver for central banks, while increasing their dependency on financial markets. Coupled with insufficient progress on structural reforms, this is likely to result in more protracted recessions in the future."

According to the analysis, Switzerland and Canada have consistently been among the top three most resilient countries over the past decade. The United States has shown a steady improvement from a low point in 2010. Last year, it ranked third, given strong economic fundamentals, efficient labor, and deep capital markets, as well as fiscal leeway to mitigate an economic shock.

By region, North America (United States and Canada) was the most resilient region in both 2007 and 2018, despite seeing a slight decline over the period. As Figure 1 shows, Latin America was the only region that recorded an improvement in economic resilience, although at a low level due to structural challenges. The region's capital markets are not sufficiently developed, labor markets show low productivity, and a significant part of the population remains vulnerable to falling back into poverty.

Figure 1: as of 5/2019 from sigma

The euro area suffered the biggest decrease in resilience, reflecting fragile fiscal positions in some countries, exhaustion of monetary policy options, a still challenging environment for the banking system, labor market inefficiencies and, in relative terms, underdeveloped financial markets. Peripheral countries in the euro area are much less resilient than the core economies, primarily because of lower fiscal resources and weaknesses in the banking sector. However, even the recovery of resilience levels in Germany and France since post-crisis lows has been non-linear and slow.

"Progressing and finalizing the European Capital Market Union will be key to improving resilience in the euro area," Mr. Haegeli said. "This would deepen financial markets and diversify the region's funding sources, taking some pressure off monetary policy. Moving forward with bank consolidation as well as overhauling labor markets are also top priorities."

Asia and Oceania had fairly stable economic resilience scores between 2007 and 2018. Resilience levels in China, Japan, and Australia improved slightly, while India's resilience declined mostly due to lower index scores for the financial-sector components, including banking industry environment, financial market development, and insurance penetration.

Micro Resilience: Measuring Protection Gaps and Insurance Coverage

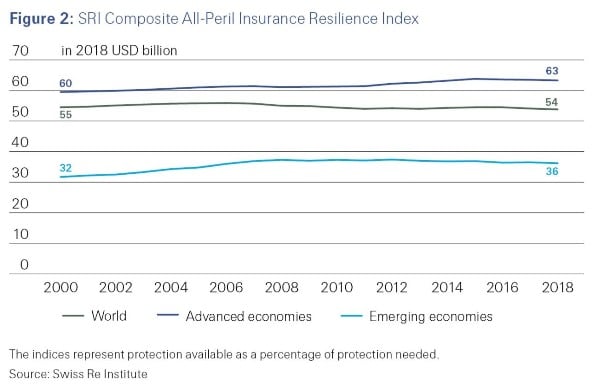

Separate to the macroeconomic indexes, SRI has also constructed Insurance Resilience Indices, based on measures of protection available relative to that needed. The indexes consider how insurance helps households withstand the following shock events: natural catastrophes, death of a household's main earner, and healthcare spending. Taking a longer-term view than for the macroeconomic indexes, SRI found that the protection gap for the 3 risk areas combined more than doubled between 2000 and 2018 to $1.2 trillion, a record high.

In relative terms, resilience has improved in most regions since the turn of the century. As Figure 2 shows, the aggregate index for the 3 perils improved in both the advanced and emerging markets, with the world index slightly lower because of the increasing economic weight of emerging markets. The key takeaways at individual peril level are the increase in aggregate advanced market resilience to natural catastrophe risks (an 8 percentage point improvement) and the strengthening of mortality protection in the emerging markets (up 9 percentage points). Notable also is the progress made in closing the health protection gap in Asia Pacific.

Figure 2: as of 5/2019 from sigma

Beyond the benefits at the micro level, risk transfer to insurance markets boosts macroeconomic resilience by facilitating stronger recovery after a shock event, sigma says. Economies with higher levels of insurance penetration also tend to exhibit less volatile growth.

Insurance Resilience in Different Regions

Europe

In Europe, the aggregate insurance protection gap amounted to $342 billion in 2018, more than double the 2000 value, with emerging countries in the region accounting for over half of the gap. However, in relative terms, the composite insurance resilience index improved in both advanced and emerging European economies since 2000.

The composite index showed a 5 percentage point improvement to 65 percent for the advanced economies in the region, meaning that almost two-thirds of all estimated protection needs from the three main risks are currently covered by existing resources including insurance. This is slightly more than for all advanced economies around the world. The biggest improvement in advanced Europe came from closing the protection gap from natural catastrophe risks, driven for example by the significant increase in the flood insurance take-up in Germany and the introduction of the Flood Re scheme in the United Kingdom.

Emerging European economies saw a 10 percentage point increase in their insurance resilience index since the turn of the century to 44 percent. The biggest improvement occurred in mortality risk protection to a level that is now roughly in line with the world average.

North America

For the United States and Canada, the composite insurance resilience index for the region improved by 2 percentage points to 65 percent in relative terms, meaning that almost two-thirds of all estimated protection needs from the three main risks are currently covered by available resources, including insurance.

Underlying the modest uptick in resilience was strong improvement in natural catastrophe protection, which increased 11 percentage points to 40 percent—the third-highest level behind Oceania and advanced economies in Europe. At the same time, mortality protection declined in relative terms, driven by developments in the United States, where wage replacement needs and debt have grown faster than accumulated financial assets and nearly stagnant life insurance coverage since the turn of the century.

The aggregate insurance protection gap for the three risk areas has increased 20 percent to $208 billion since the turn of the century.

Latin America

In Latin America, the aggregate insurance protection gap was $103 billion in 2018, about 40 percent higher than in 2000. In relative terms, the composite insurance resilience index edged up by 3 percentage points to 37 percent, meaning that almost two-thirds of all estimated protection needs from the 3 main risks are currently not covered by available resources, which include insurance.

This level is well below the world average resilience score of 54 percent but in line with the overall emerging market aggregate of 36 percent. By risk area, health insurance coverage improved substantially since 2000, increasing 10 percentage points to 89 percent, the strongest level among all emerging economy regions. By contrast, the coverage of mortality and natural catastrophe risks has remained at a very low level.

Asia Pacific

In relative terms, the composite insurance resilience index improved in both advanced and emerging countries in Asia Pacific (APAC). The largest improvement in insurance resilience was in Oceania, where the index increased by 18 percentage points since the turn of the century to 77 percent, making the region the most resilient geographic area by far. Oceania also has the highest resilience score for natural catastrophe risks of any region in the world at 69 percent. This reflects compulsory earthquake covers in New Zealand and success in efforts to increase uptake of flood insurance in Australia.

In the rest of advanced APAC, the composite insurance resilience index was up 4 percentage points to 59 percent, while for emerging economies in the region it rose 7 percentage points to 31 percent. Advanced APAC countries have the highest insurance resilience score for mortality risks of any region globally at 62 percent. Taiwan, Hong Kong, South Korea, and Japan are among the economies with the highest life insurance penetration in the world, driven by savings-type products.

In emerging APAC countries, insurance protection against the main three risks continues to be at significantly lower levels compared with advanced-economy counterparts. One notable development in emerging APAC is the strong gain in resilience against healthcare spending risk, reflecting the major universal health coverage-inspired reforms that have been implemented in China, India, Indonesia, Philippines, Thailand, and Vietnam.

Emerging economies in APAC have the largest absolute insurance protection gap of $456 billion, representing almost 80 percent of the region's total of $572 billion.

SRI-LSE Macroeconomic Resilience Index, 2018 ranking by country, and index scores (2018 and 2007) sigma 5/2019

September 09, 2019